Alaska

Alaska is reportedly considering a tax-based LTC program. The median age of Alaska's population is low, but Alaska has the highest cost-of-service in the U.S. by a large margin.

California

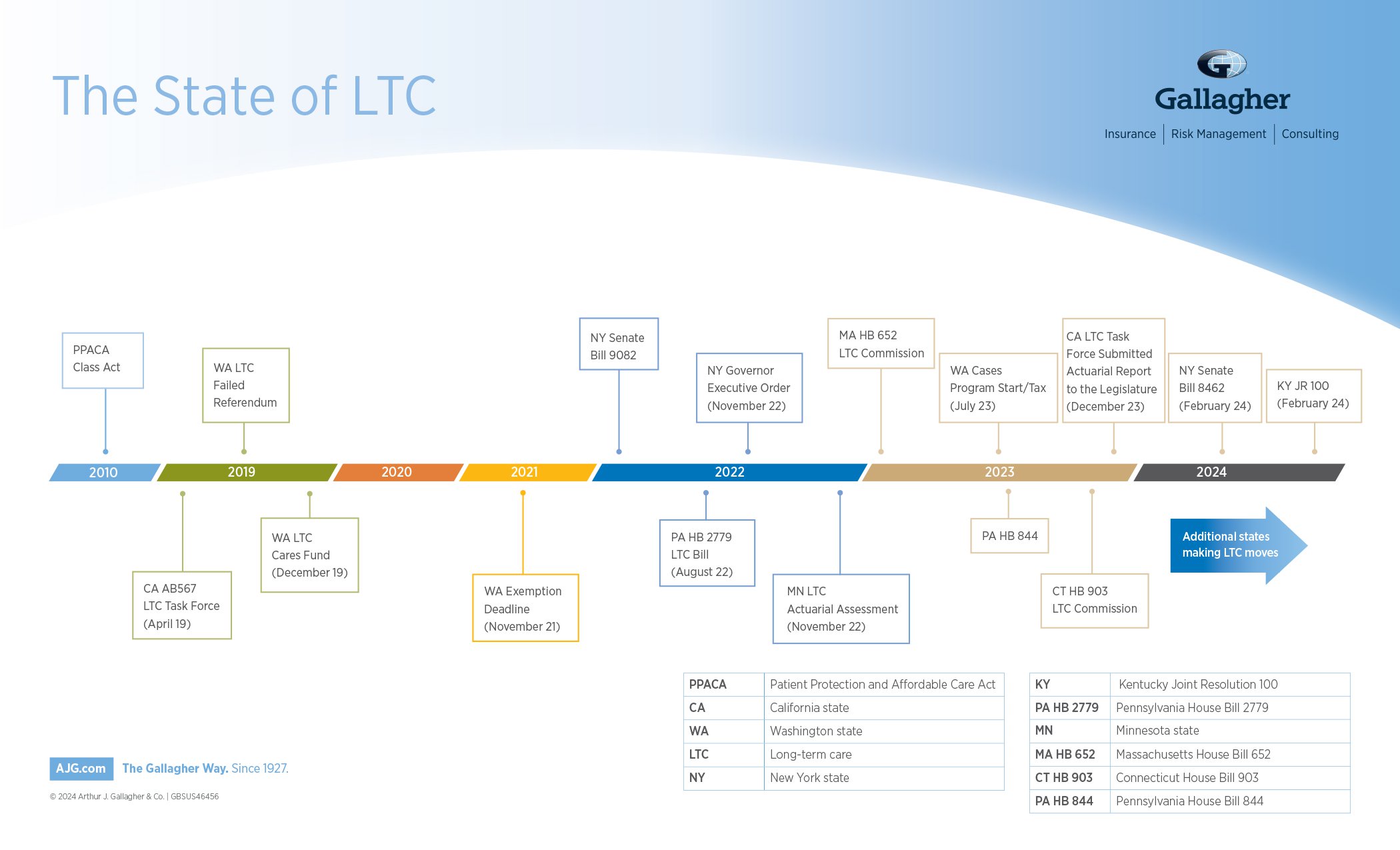

California adopted CA in 2019 (AB 567), which established California's Long-Term Care Insurance Taskforce "to explore the feasibility of developing and implementing a culturally competent statewide insurance program for long-term care services and supports."

The last scheduled meeting of the task force was held on December 18, 2023. The task force discussed and approved the finalized actuarial report of its recommendations for a state LTC insurance program. The proposed program design recommendations are non-binding and advisory only, and no state plan will go into effect in California unless the California Legislature takes legislative action to enact a plan. Furthermore, please note that the report is solely that — a report. If California legislators decide to consider a bill, they can take any/all/none of the report into consideration. It doesn't mean that a proposed bill will mirror any report details.

In the report, the task force identified five options for program design that vary on several plan components and conducted an actuarial analysis of each design. Ultimately, the California Legislature, if inclined, will assess the options and may choose to adopt some or none of them. Until then, these recommendations provide a foundation for future legislative action but don't require it. Similarly, there's no timeline by which the legislature must act upon these recommendations. As a result, the legislative process will govern if and when a bill is introduced, and, if introduced, whether and how it may proceed. Until then, any potential program details remain unknown and speculative.

While the role of private long-term care insurance was discussed throughout the task force process, it's premature to speculate about what role private insurance may play in any plan the legislature might adopt, including key details such as effective date or types of qualifying coverage.

The task force agreed that meeting with the legislature was the most important next step. The California Department of Insurance agreed to include language in the actuarial report prompting the legislature to meet with interested parties and the California Department of Insurance to explain and complete some of the missing topics of consideration. The response from members of the legislature will dictate additional next steps for the task force.

No legislation to establish a state run LTC program was introduced prior to the February 16 deadline to introduce legislation for the 2024 session.

You can access the Actuarial Report, meeting notes and additional information on the California Department of Insurance website.

Colorado

Colorado is reported to be considering a tax-based LTC program. Colorado House Bill 1122 was introduced in 2023 and called for a tax credit for purchasing LTC Insurance. The bill failed to pass out of committee.

Hawaii

Hawaii has attempted to move LTC legislation forward several times, without passage. Currently, no specific legislation is being considered. It's reported that the state continues to assess the need, given its population's above-average median age. About one third of state revenues are tourist based, so sales tax might be apportioned instead of a new payroll tax.

Maryland

Both House Bill 249 and Senate Bill 631, introduced in 2024, were withdrawn by their legislative sponsors. No study legislation will be considered during this session.

Massachusetts

Bill HD.2610 was filed on January 19, 2023 but has not been introduced or voted upon. This resolution would establish a long-term care subcommittee that would steer action surrounding an actuarial assessment similar to California's task force project.

Funds were approved in August 2023 for actuarial study. A bill to create the LTC task force was favorably reported by the Joint Elder Affairs Committee and has been referred to the Joint Rules Committee.

Bill H.2610 shows the progress of An Act Establishing a Special Commission on a Statewide Long-term Care Insurance Program.

Minnesota

The initial report recommends integrating private insurance into the three options despite limited consultant receptivity to concerns about carriers' hesitancy towards one-state solutions. The likelihood of enacting "transformational" funding options in 2024 seems slim due to a short legislative session and challenges in personnel recruitment for 2023 initiatives. The report proposes a measured approach, starting with the care coordination website and potentially incorporating the market-based Medicare coordination product, gradually progressing to more transformative funding options.

New York

The New York Long-Term Care Trust Act, Senate bill 9082, was introduced to the floor in May 2022 and moved to committee. It was largely modeled after the WA Cares Act. Any additional legislative action will require the bill to be re-drafted and/or re-introduced. Given that New York has a Democratic governor and a Democratic supermajority, any new bill that gets traction is likely to pass. The issue of LTC has significant attention because of the number of COVID-related deaths in nursing homes in 2020 and 2021. Their "Master Plan for Aging" council is to develop a report for the governor by January 1, 2024.

New York State Senate Bill S9082 shows the progress of the New York Long-Term Care Trust Act.

Pennsylvania

House Bill 2779 was introduced to the floor in August 2022 and moved to committee. It uses elements of the WA Cares Act, including a payroll tax of 0.58%. The bill didn't move forward but, with Democrats newly in control of the legislature and a Democratic governor, Pennsylvania is a state worth watching.

Pennsylvania House Bill 2779 shows the progress of the Long Term Care Trust Act.

Washington

The WA Cares Act passed, and tax collection begins July 1, 2023. The legislature will be presented with new elements/amendments to consider pertaining to exemptions, portability and eligibility. But now that the state's actuarial analysis projects solvency for 75 years based on current provisions, it's unlikely anything significant would be added that would impact these projections. The window to obtain exemptions for private insurance holders ended in November 2022. Benefits start in 2026.

Washington state ballot initiative 2124 to amend the Washington Cares Act will appear on the November ballot.

WA Cares has links to monthly webinars about aging and caregiving includes how WA Cares relates to that month's topic, sign up for the WA Cares newsletter, find FAQs and more.