Author: Adnan Arain, J.D.

While D&O policies address the acts or omissions of directors, officers and even employees, D&O policies sometimes leave employed lawyers, such as general counsel or staff attorneys, outside the scope of coverage. For this reason, companies should consider purchasing employed lawyers coverage (EL coverage). This advisor discusses EL coverage, and specifically in the context of purchasing it alongside directors and officers (D&O) coverage, either as a sublimited enhancement or as a stand–alone limit.

Consider the following scenario: An employed attorney of a company agrees to participate in a panel discussion along with other business leaders. Despite the benefit of an in-house attorney participating in a panel discussion, the attorney may inadvertently cause damage by doing so. This can come in the form of damage to their company, if the attorney discloses confidential information, or an audience member may misconstrue their speech as legal advice to be relied upon—to their detriment.

The EL insurance policy may respond to these scenarios by extending legal malpractice insurance to lawyers performing legal work for their sole client-the company that employs them. These lawyers can be sued by third parties, vendors, or even shareholders or board members for their legal acts or omissions. Subject to the policy's conditions and exclusions, and excess of a self-insured retention, EL insurance would cover both defense costs and final settlement or verdict.

Filling Potential Gaps

Within the D&O context, employed lawyers insurance often fills an important gap: The general counsel may qualify as a covered executive, but may not be insured for legal malpractice they commit in their role as general counsel. One reason for the shortfall in coverage is that certain D&O policies specifically exclude professional services. Additionally, other employed lawyers of the organization, hired to perform job duties in their capacities as practicing attorneys, do not qualify as executives under the D&O policy. These employed attorneys often remain left out of any specific grant of cover. Employed lawyers coverage fills this potential gap by setting forth an exception to any professional liability exclusion for the acts of an employed lawyer.

Thus, in a complaint, the plaintiff may list the employed lawyer as a named defendant, alleging damages due to the legal malpractice committed by the individual attorney. The employed lawyer would seek indemnification from the entity per the company's founding documents (and possibly per the company's employment agreement with the attorney) and in accordance with any applicable state statutes. The entity would indemnify the employed attorney where appropriate, and would then notify a claim against its EL policy.

Beyond these basic principles, the types of available EL policies differ significantly, from very broad coverage to relatively limited coverage and a number of variations in between.

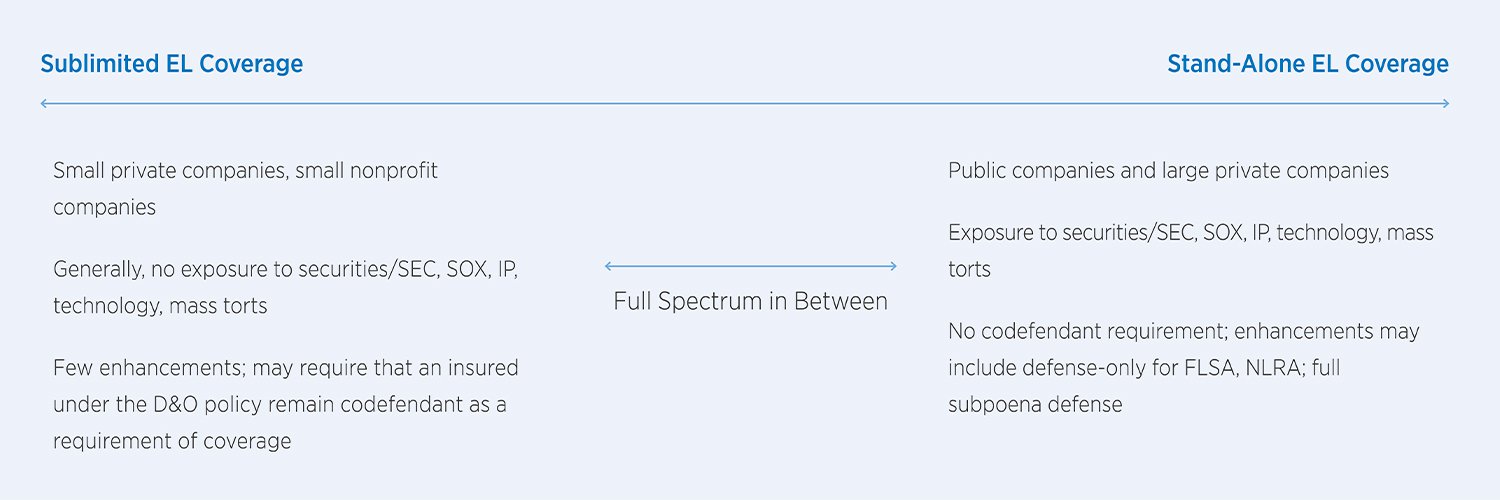

Sublimited Employed Lawyers Coverage Under a D&O Policy

The more limited variety of EL coverage costs either a minimal premium or no additional premium when added to a D&O policy. But this form of EL coverage also offers no additional limit-it merely sets aside a sublimit to cover employed lawyers. Insurers typically add sublimited EL coverage as an enhancement on smaller, less complicated accounts.

This variety of EL coverage typically limits coverage to acts performed within the scope of their roles as employed lawyers only, and specifically excludes (1) legal work performed for any client other than the employer (often deemed moonlighting), and (2) pro bono legal work, even if it somehow benefits the employer.

This variety comes with other important limitations, as well. It defines an employed lawyer as any employee who is or was admitted to the practice of law at the time of being hired. This variety of the coverage also may require that the employed lawyer be part of the general counsel's office, meaning that attorneys working in finance, risk management or human resources would not qualify for coverage. Importantly, the more limited version limits coverage to attorneys only, and not, for example, the paralegals, legal secretaries or other staff members working with the employed attorney.

Lastly, some insurers impose the additional condition that a non-attorney insured individual be a codefendant in order for the EL coverage to apply. The rationale for such a rule is that the core insuring agreement of the D&O policy still applies. This way, the EL sublimit is only deployed when the D&O policy is responding to claims that would be covered in absence of the EL enhancement.

Stand-Alone Employed Lawyers Coverage

By comparison, a more impactful version of EL coverage is available for an additional cost and provides its own dedicated limits. Intended for larger or more sophisticated risks, stand-alone coverage takes the opposite approach as compared to the sublimited coverage described above, by extending a more broad coverage in a number of ways.

First, it specifically covers both work done for a client other than the company employing the attorney (known as moonlighting) and pro bono legal work. This may represent an acknowledgement that certain companies value having employed attorneys volunteer their time to worthy legal causes. For example, the insured company may place a premium on attracting conscientious legal talent who are dedicated to social causes, especially in the era of environmental, social and corporate governance (ESG) awareness.

Within certain guidelines, companies may even value having their attorneys provide legal advice or input within the broader business community, or to coworkers. Even where an entity forbids its attorneys from giving legal advice to others, this will not stop a third party from bringing a claim, such as a counterparty to a negotiation or a non-client who relied on the incorrect advice of the attorney. Even if such claims were ultimately proven frivolous, stand-alone EL policies would fund their defense and, in most cases, verdicts or settlements, excess of a self-insured retention.

Similarly, stand-alone coverage may not require that an employed lawyer be part of the general counsel's office. Thus, an employed lawyer who works as a consultant or who uses knowledge of employment law in the role of an HR executive may be covered for acts that would purportedly qualify as the practice of law.

Stand-alone employed lawyers L extends coverage to the legal staff as opposed to merely the employed attorneys, in essence recognizing that legal errors resulting in damages may arise from the acts of paralegals or legal secretaries. And, given the stand-alone nature of coverage, there is no requirement that any other line of coverage be triggered in order for EL limits to deploy.

Similarly, insurers of the stand-alone product can add additional enhancements. These may include defense-only costs for malpractice claims alleging violations of various statutes (these causes of action may otherwise be excluded under a D&O policy): wage and hour allegations under the Fair Labor Standards Act; legal services addressing unions, unionizing or similar issues under the National Labor Relations Act; or violations of COBRA or OSHA. Insurers may also include subpoena defense coverage for legal malpractice claims against the employed lawyer.

Employed Lawyers in the Context of Severity and Litigation Trends

Given the overview of the more narrow sublimited coverage and the more robust stand-alone coverage, the size and sophistication of the risk can serve as a rough guide as to which option to choose.

Larger and more sophisticated clients are more likely to see the value in the stand-alone coverage. The employed lawyers of public companies, for example, are subject to Sarbanes-Oxley requirements regarding the company's financials. Unlike smaller private companies, public companies would inevitably deal with securities law issues. Their in-house attorneys would, at the very least, oversee outside firms practicing securities law. Even large privately held companies may provide goods or services related to higher-severity areas of practice such as technology, intellectual property and toxic torts. A legal malpractice claim against an employed attorney in any of these areas of practice could result in high-severity losses.

By comparison, companies with smaller revenues, or nonprofits with smaller asset sizes whose attorneys do not practice in a high-severity area of law, may opt for the sublimited enhancement to its D&O policy. This approach would remain consistent with not only lower risk profiles but also smaller risk management budgets.

There are exceptions to the general rule that size will correlate to a preference for stand-alone coverage. For example, an independent private equity sponsor may have a small revenue size, but may effectively control a private equity portfolio. Similarly, while a boutique start-up advisory firm may not be large in terms of revenue, it may advise large and sophisticated clients on tax or merger and acquisition issues. The most successful tech start-ups may start out with relatively low revenues but scale up dramatically. Smaller companies focusing on research and development, in the pharmaceutical space for example, may similarly start out with relatively small revenues while having the potential for high-dollar claims. Given the potential of high-severity claims, employed attorneys in these scenarios may be better served with stand-alone coverage.

Additionally, the past decade-plus has brought an increased litigiousness and, specifically, an increase in third-party claims against lawyers i.e., claims by non-clients against attorneys for legal malpractice. As mentioned above, an audience member may sue for malpractice after misconstruing public statements of an attorney as legal advice, or a business partner may sue for representations made during a negotiation. Other background trends in litigation generally, such as rising defense costs and social inflation of verdicts or settlements, would apply to legal malpractice claims, as well. These trends may influence the buyer to lean toward the more robust option with regard to employed attorneys.

For more information on employed lawyers insurance, please contact your Gallagher representative, or Adnan Arain at (312) 803-6342.