Author: Heidi Roberts

Introduction

Although the events of 2021 may not have been as unexpected and dramatic as 2020, it is unlikely that we could have predicted the length of the ongoing pandemic and supply chain issues that impact our clients, especially those in the private and nonprofit sectors.

What we saw in 2021

Since the financial condition of the insureds heavily impacts Directors & Officers (D&O) underwriting, when looking at our private and nonprofit D&O insurance clients' financial conditions, there appeared to be three main situations:

- Those who operated at a loss, closed their doors or filed for bankruptcy

- Those who were fairly stable

- Those who flourished so much that they acquired other entities and went public

There are still far-reaching implications on D&O for the first and last categories since the directors and officers of these entities had significant decisions to make.

Market response and underwriting process implications for private and nonprofit D&O insurance coverages

Although there is still a high degree of underwriting scrutiny, it appears to have lessened since this time last year. However, we still face markets:

- Requiring additional information aside from the typical application and financial statements, but also questionnaires regarding continuity plans, return to the workplace, vaccine mandates, etc.

- Reducing limits

- Increasing retentions

- Eliminating additional D&O Side A limits

- Adding exclusions like antitrust, insolvency and infectious diseases

We also saw changes in underwriting philosophies based on the class of business. Although it was not as prevalent in 2021 as in 2020, some markets had to adjust their renewal terms if they were exiting a certain class of business or had to get off a risk due to increased exposure. We also were faced with high underwriter turnover that further complicated some of these situations.

Some clients wanted to either increase limits due to increased exposure or reduce limits to save premium due to their financial constraints. Gallagher has continued to find creative ways to reduce premiums and offer alternative options since D&O coverage is even more critical than ever to protect the directors and officers of private and nonprofit organizations. As always, you should connect with your broker and risk management team to understand the nuances of your business.

Current state of the market

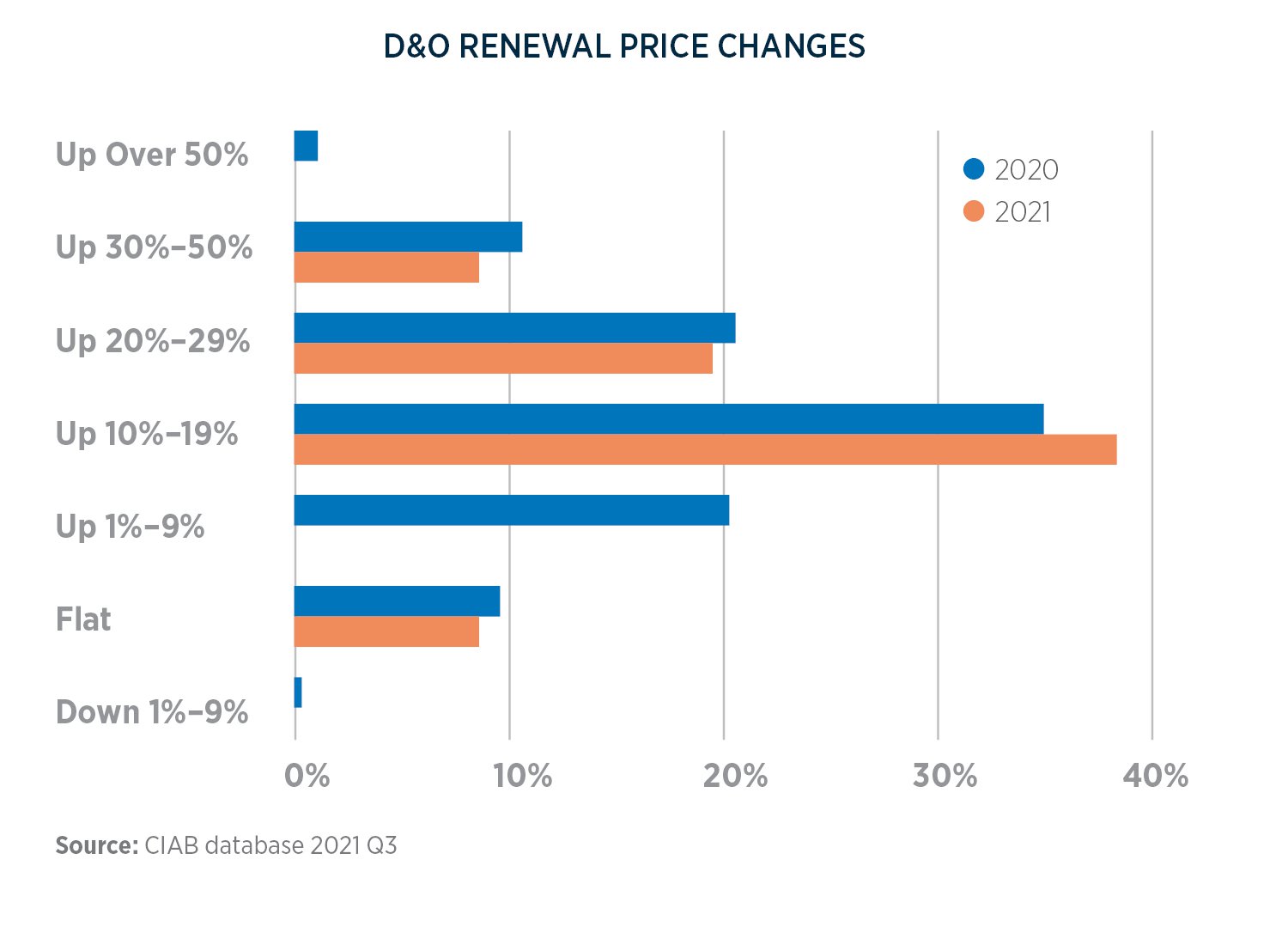

In addition, we generally still saw private and nonprofit D&O renewal rate increases, but they were not as dramatic as what we saw in 2020, for the most part.

D&O RENEWAL PRICE CHANGES

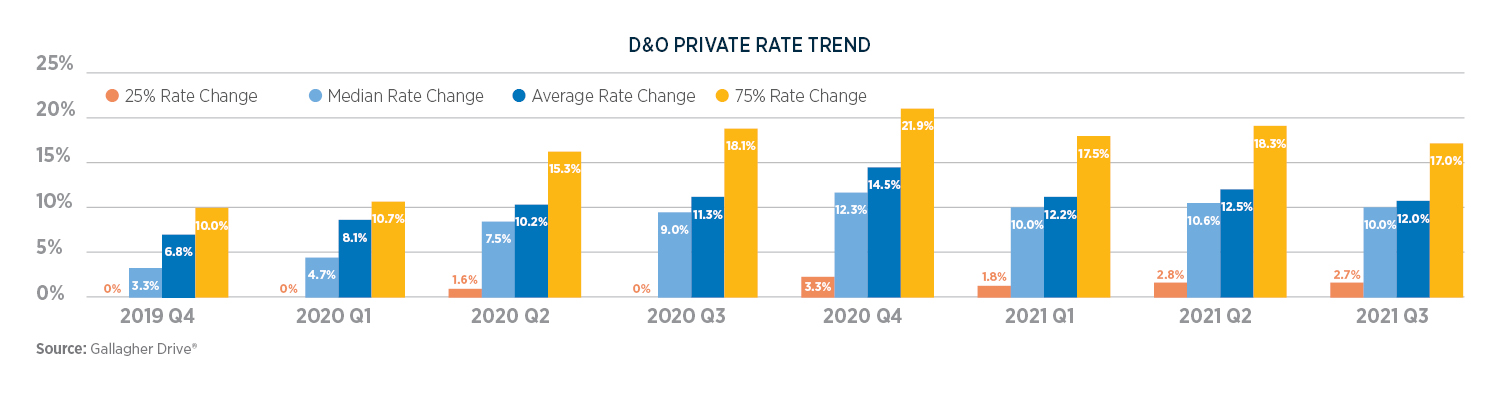

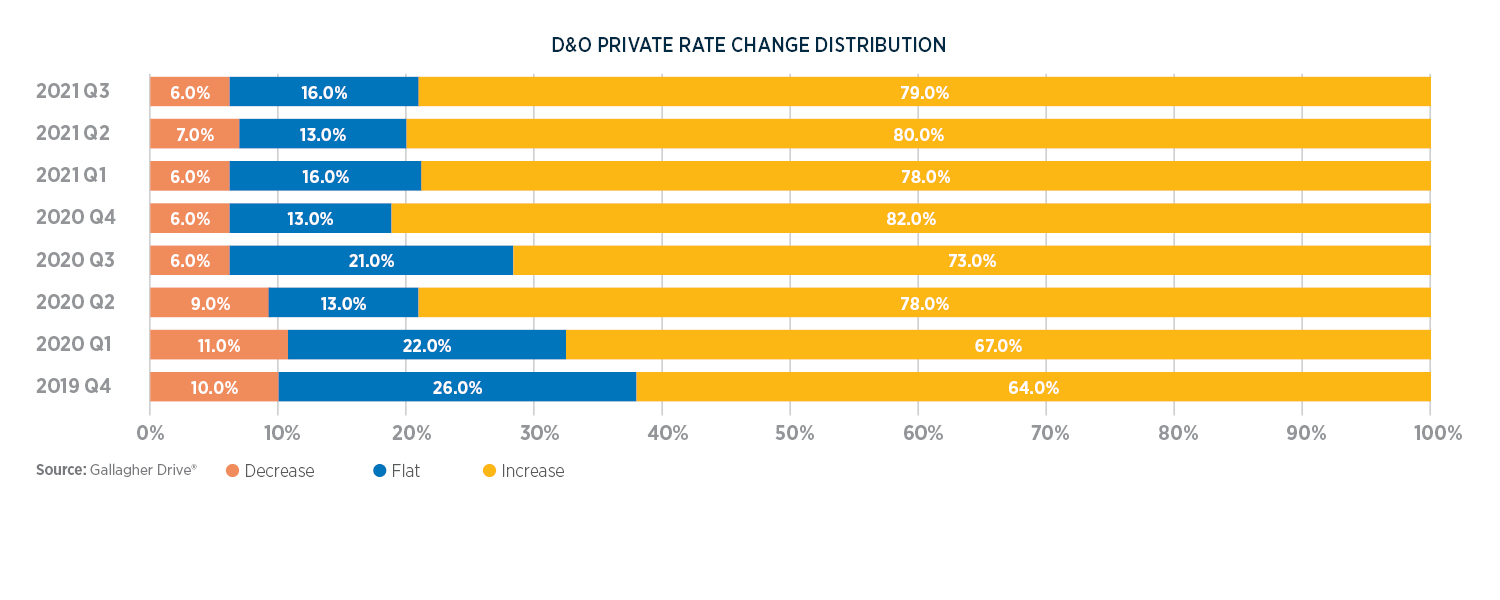

Our proprietary data and analytics platform, Gallagher Drive®, is available to private D&O clients. By utilizing Gallagher Drive®, our brokerage team can provide specific rate guidance for your line of coverage, industry and geography. Combined with deep expertise in your particular industry and business, Gallagher can help you navigate today's highly nuanced market for D&O insurance for private and nonprofit organizations.

Our data in the graphs below show that the rate increases peaked in Q4 of 2020 and started to decline in 2021.

D&O PRIVATE RATE TREND

D&O PRIVATE RATE CHANGE DISTRIBUTION

Claim trends

There is a longer tail on D&O claims, with insurance companies still paying out losses from claims that occurred during the previous financial downturn. Given the broad entity coverage provided under private and nonprofit policy forms, insurers often find themselves paying more claims as well as more expensive claims, which makes them especially concerned with the long tail of these claims. We also know that more insolvencies and bankruptcies often result in more D&O claims. This is also the case with mergers and acquisitions. Therefore, whether a client's business floundered or flourished, there is more likelihood for claims for these scenarios.

We have also seen our nonprofit clients, especially social services organizations, be tasked with having to do even more with even less. Nonprofits working with youth and vulnerable populations are targets for legacy liability. Given the legacy risk of alleged negligent oversight from older claims (latent nature of this exposure) and the value of time and resources to better understand this risk today, these nonprofit organizations need to prioritize best-in-class risk management with board oversight. So given the market conditions, it is essential for clients who have experienced claims to be prepared to let the underwriters know what they have done to decrease their exposure.

Crossover claims are also more prevalent with D&O insurance coverage, and we see this most with cyber insurance coverages and employment practices liability (EPL) insurance coverages, in particular.

Key cyber coverage considerations:

- More discussions are being held with clients regarding the implications of security and privacy liability on D&O as the frequency of ransomware attacks and cyber liability claims has increased. We also see this heightened with more employees continuing to work remotely — even if this is part-time.

- A cyber claim can cross over into D&O when there are allegations that the directors and officers did not put the proper safeguards or coverage into place.

- There are more first-time buyers of D&O due to the heightened awareness of this coverage and the fact that smaller organizations are more able to afford it.

Key EPL coverage considerations:

- The #MeToo movement and heightened awareness of social issues, such as discrimination, have increased the likelihood of EPL claims.

- One may think that EPL claims may not occur with much of the workforce working from home, but that is incorrect. There is decreased supervision, more furloughed or laid-off employees, and those employees who make complaints against their employers may feel that they are being retaliated against.

- EPL insurance is a distinct and well-established coverage. We can see that decisions made by directors and officers about their workforce may be called into question and could result in reputational damage. We see this as some clients have returned to work and have vaccine mandates.

Looking ahead

Although the pandemic has not ended, a lot of the marketplace volatility has ended or waned. As a result, we project that, on average, there will be 5.0% to 20.0% rate increases for private and nonprofit D&O clients with minimal changes to the risk of the markets.

Conclusion

D&O coverage is crucial when management is tasked with making more decisions and more complicated decisions than usual. So even though clients may be facing financial constraints and may be tempted to discontinue their D&O insurance coverage or reduce limits, now is not the time to do so. Because of the highly nuanced nature of this market, it is imperative that you are working with an insurance broker who specializes in your particular industry or line of coverage. Gallagher has a vast network of specialists that understand your industry and business, along with the best solutions in the marketplace for your specific challenges.

Please note: A client's risk profile is the primary variable dictating renewal outcomes. Loss experience, industry, location and individual account nuances will also have a significant impact on these renewals. Many risk characteristics influence these results, such as significant changes in ratable exposure, any type of liquidity or significant debt issues, presence in California and other higher-risk areas, claims history, nature of operations, and size where they can see increases over 50.0%. That is why it is even more important to have discussions ahead of time, as much as possible, so that you can make an educated decision about this crucial coverage.