The volatility of the market is more pronounced now than it has been in the past 17 years. Capacity has been cut dramatically; there is around one third of the limit available on any given risk versus the levels of available capacity in 2015-16. Pricing and retentions have materially increased. There is now a very real threat of programmes not being renewed, or clients being required to self-insure some layers. Given these current trends, we do not expect these conditions to improve for the better in 2019.

Trouble across the board

Virtually every aspect of the Directors’ and Officers’ (D&O) market has been affected, from private companies through to the largest multinational, publicly listed companies. The Crime market has suffered even more; further withdrawals of markets means that there now only remains about GBP20m of available capacity for full Social Engineering cover.

At the time of writing, management liability underwriters are going through a torrid time.

- The deterioration of past claims continues unabated, with underwriters posting higher and higher reserves on old claims that were previously assumed to be contained within primary layers.

- Constant elevated levels of securities filings all put pressure on the primary carriers. One bright spot is the level of dismissals of these class actions.

- Lloyd’s of London’s increased regulatory focus and scrutiny of the profitability of specialist classes has led to underwriter constraints and in extreme cases, insurers refusing to renew business for period of time.

- The number of crime losses continues unabated. As a result, we are seeing some insurers refusing to pay claims for losses that previously would have been covered.

Unfortunately, during this hardening of the market we have seen some pockets of unfavourable insurer behaviour and as such, market selection will need to be even more strategic and forward- thinking at renewal.

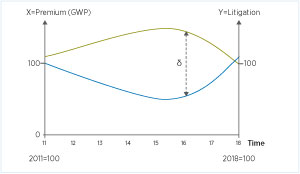

As the diagram shows, 2016 will mark the high point in losses for the D&O market. Whilst during 2018 heavy remedial action was taken by insurers, it is doubtful that despite this action, insurer behaviour will not readjust until the market is more profitable.

So what can be done in 2019 to mitigate this environment?

- Insurer arbitrage: Not all insurer offices or individual underwriters behave in the same way. It is important that clients choose to work with the most appropriate underwriters for their risk profile, so that at renewal, the optimal terms can be achieved. Your broker will guide on this.

- Game theory: In order to build significant programmes with the most favourable terms and conditions, brokers must employ game theory strategies to leverage insurers whilst maximising competition and capacity.

- Programme design: Design of programmes in 2019 must be creative; retentions, side-A layers, ventilation, and changing the overarching structure can help. In addition, the use of small lines of GBP1m-2m has become increasingly useful for very difficult placements.

- Worldwide marketing: The utilisation of the full gamut of international insurers will be vital at renewal. European markets, plus those in the US and Bermuda can all provide options for clients as those markets have not hardened as quickly as London.

What does this mean for renewals?

Buyers in 2019 are now likely to observe the harsh reality of a hard market; rate rises upon renewal, restrictions on coverage, additional exclusions, and potentially challenging claims experiences. Insurers are undoubtedly being more selective of the risks that they are choosing to write, preferring to decline a risk entirely if it falls outside of their underwriting appetite, as opposed to writing risks to maintain a portion of market share.

Top tips

Those businesses that are renewing their programmes during 2019 will need to work closely with their insurance brokers, and take some proactive, practical steps to prepare for these new market conditions:

- Engage with brokers and insurers: Our key piece of advice is to engage with your broker early. In a hardening market insurers do refer risks ‘up the chain’ to senior underwriters, or above, as they become more selective or as they try to manage underwriting directives from their boards. Push your brokers and insurer hard, gather your information in plenty of time, and expect insurers to ask more questions than usual.

- Consider insurers and underwriters: As insurers become more selective, you should consider all possibilities. Every underwriter is different; unsurprisingly those which are more experienced and knowledgeable will give clearer rationale on their decisions, and invariably will provide the best terms. Your broker will be able to advise you on the most suitable, alternative choices of insurers and, crucially, will ensure that the selection is aligned to your requirements.

- Leverage insurer relationship: This can increasingly help obtain crucial capacity and complete difficult placements.

- Global marketing: No stone must be left uncovered. All possible capacity should be approached and all options sought out.

All of the above will help, although it will not alleviate in full the broader challenges of a hard market renewal. Clients must work closely with their brokers, particularly for those renewals falling in the first half of 2019, to prepare as far as possible for what will inevitably be a difficult renewal period.